Professor Tim Congdon CBE is a member of The Bruges Group Academic Advisory Council

A lot of interest has been drawn from my recent emails to my fellow macroeconomists and monetary analysts where I pointed out that bank deposits at US commercial banks soared in the fortnight to 25th March. We now have the US commercial bank data for another week, that to 1st April, as well as an estimate (from Shadow Government Statistics) of M3 growth in March. This special e-mail is to provide another update on the latest monetary developments.

In the week to 1st April bank deposits at US commercial banks rose by 1.0%, less than half the rate of increase in the two previous weeks, but still very fast by normal standards. (1.0% a week implies an annualised rate of increase of 67.8%.) In the three weeks to 1st April – roughly speaking, the period since the announcement of the national emergency by President Trump on Friday, 13th March – these deposits went up by 5.8%. (The implies annualised rate of increase is 165.0%.)

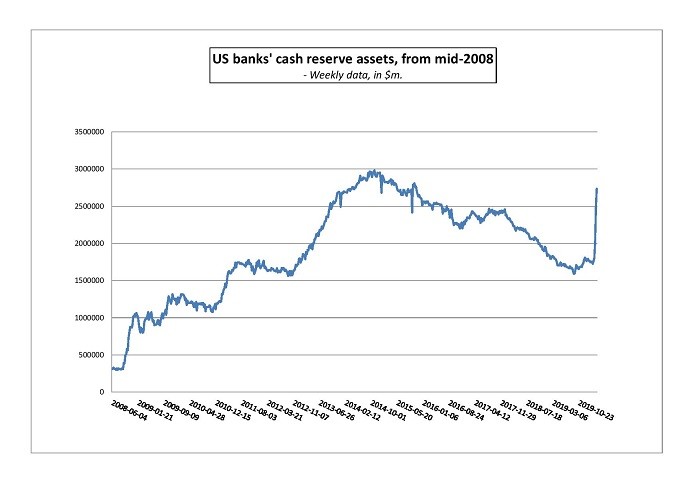

The explanation for the 1.0% gain in the latest week is to be sought in the Federal Reserve's asset purchase (or "quantitative easing") programme and/or direct Federal Reserve financing of the budget deficit. Commercial banks' own credit extension was not remarkable and a surprise is that their holdings of US Treasury securities actually declined. The big addition to banks' assets was in their cash holdings which jumped in the week from $2,490.8b. to $2,734.3b. The chart below shows how these cash holdings have surged in the last three weeks. The steepness of the climb is impressive, compared notably with that seen in the three instalments of QE from 2008 to 2014.

According to Shadow Government Statistics, the USA's M3 measure of money went up by 3.9% in March. In one of recent e-mails I suggested that deposits might on average be $200b. higher in April than at the final March date (i.e., that for 25th March) and that this would be consistent with a 4% - 5% jump in M3 in April. (In the USA the monthly money number is an average of all the weekly numbers, not an end-month value.) Deposit in fact went up by $140.5b. in the first relevant week of April, which is not inconsistent with my conjecture, but argues that I may have been too cautious. If deposits keep on rising by $140b. a week, the growth between the months of March and April would be 5%, and that of M3 would be similar. So we would have M3 money growth rates in the three successive months – February, March and April – of 0.5%, 3.9% and 5.0%. The consequent annualised rate of increase in the three months would be almost 45%.

I would expect very fast money growth to persist in May and June, and perhaps for somewhat longer, because,

1) The 2020 US Federal deficit of $3,000b. - $4,000b. may fall particularly in the March-June period, but it will still be well above the 2019 level through to spring 2021, and to a significant extent it will be financed from the Federal Reserve and the commercial banks

2) Programmes to improve credit availability to cash-starved corporates have been announced, and will be causing additional and well-above-normal bank credit for a few quarters yet. (The programmes include the Primary Market Corporate Credit Facility, mostly for large, investment-grade companies; the $350b. Small Business Administration loan programme; and the Temporary Corporate and Small Business Liquidity Facility, with potentially $1,000b. of loans, backed by $85b. of US Treasury capital, with the loans perhaps lasting five years and carrying an interest rate of 2¼%.)

Having said that, it seems plausible that the peak money growth in this episode will have been in March and April 2020. As before, my central view is the US broad money growth in – say – the year to late 2020/early 2021 will lie in the 15% - 20% band and could be the highest in US peacetime history.