Taxation without representation

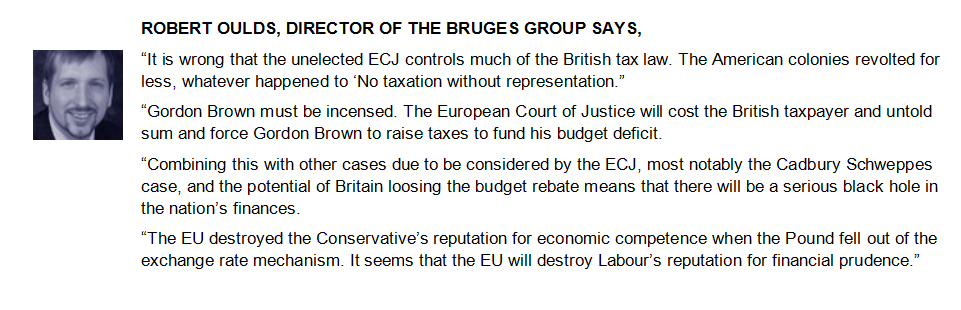

Robert Oulds

Press Release

For Immediate Release

EU forces changes to British tax law

THE MARKS & SPENCER CASE

The European Court of Justice and Taxation

Today the ECJ ruled on British tax law. The long awaited judgement from the unaccountable ECJ could cost the British taxpayer billions of Pounds. The fact that the EU has overturned UK tax law shows that Blair’s famous red-line, which he claimed he secured when the EU Constitution was being drafted, was in fact a red-herring. British governments had already surrendered the UK’s right to determine about 20% of this country’s taxation.

The Bruges Group have been warning the Government for many years as to what might happen. Now Blair and Brown will learn, but this will be a lesson learnt at the taxpayers cost.

The decision today shows that the EU has usurped the right to make UK tax laws. The ECJ has struck-out well-established UK rules in pursuing the Brussels goal of tax harmonisation. This will cause uncertainty for business and government funding. The government has known about this risk since at least 1999, and should now act to bring back control of the UK’s tax affairs.

Chillingly the ECJ has ruled that,

"The Court reiterates, first of all, that although direct taxation is within the competence of the Member States, the latter must exercise that competence with respect for Community law."

The treasury has so far refused to reveal the extent of the costs of this judgement.

Other areas of UK tax law under assault from the EU are:

- overseas dividends,

- transfer pricing,

- anti tax-haven legislation (Controlled Foreign Company tax),

- taxation deducted from savings income (Withholding tax),

- the rules governing the use of tax losses belonging to one UK company to other companies in the same group (Group relief),

- rules that prevent overseas owned companies getting UK tax relief for excessive interest payments to their parent, (Thin Capitalisation).

Areas already under the control of the EU are:

- VAT

- where tax is triggered when people seek to move assets offshore and would otherwise be able to dispose of them tax-free,

- taxation of dividend income received from overseas companies,

- and those laws that prevent UK subsidiaries of groups based in other EU states obtaining tax relief for artificially large interest payments on loans from their Parent Companies.

- ENDS -

Notes for Editors

Click here to obtain full details of the ECJ's ruling>

Current British tax law

Group Relief is available between companies that are either UK resident or have a branch subject to corporation tax in the UK, and which are under 75% common ownership.

Group relief works by the company with losses surrendering them to the company with profits, who then uses those losses to reduce their own corporate tax bill.

This law has been in existence in the UK since the 1960s at the latest.

Case history

The Marks and Spencer v Halsey case arose from M&S seeking to surrender losses of French, Belgian and German companies against the profits of their UK companies for years in the mid-90s. M&S are unable to do this under UK statute but are claiming under Article 43 (Freedom of Establishment) and Article 56 (Freedom of Capital) that the rules that prevent them doing so are discrimination under the EU Treaty, as it favours the establishment of business and capital in the UK rather than in other member states. Tax laws that are so discriminatory are then regarded as invalid under the law of the relevant Member State.

1. Today’s judgement follows a line of cases held by the European Court of Justice since the 1999 case of ICI v Colmar. These cases, taken from many Member States, potentially strike out direct tax provisions including transfer pricing, controlled foreign company, group relief, thin capitalisation, taxation of dividend income, payments into pension schemes and migration, and effectively this judicial law-making is forcing member-states to have a common tax base.

2. The M&S case was originally heard at the Special Commissioners in 2003, where the court held in the Inland Revenue’s favour, on the basis that the difference in treatment of overseas subsidiaries, was a difference, and that not every difference was necessarily discriminatory, eg in M&S' case there was a corresponding benefit to the disadvantage in that the overseas subsidiaries’ profits would not be taxed. M&S appealed to the High Court, who referred the matter to the ECJ as it required an interpretation of unclear European law. The Advocate General opined in M&S’s favour in Spring 2005.

3. No-one, with the exception of HM Treasury and government ministers, knows the quantum of UK tax at stake in respect of all the EU cases, Accountancy Age estimated it to be approximately £20 billlion. Tax refunded in respect of prior years will also include interest due to the taxpayer from the time when the tax payment for the relevant year fell due.

4. HM Treasury has constantly refused to answer the question when tabled in the House of Parliament, the reasons given including that it may be prejudicial to relations with multinational bodies, and it would increase the cost of government debt.

5. UK tax law is also under assault from corporates taking the government to the ECJ in respect of transfer pricing, taxation of overseas dividends, controlled foreign company rules (UK anti-tax haven laws), tax credits on pre-1997 dividends paid from non-UK EU companies, overseas leasing.

6. UK corporates have claimed back tax paid in previous years on the basis that the existing taxing provisions of UK law were contrary to the EU treaty. These claims are thought to go back as far as 1973, but most start in the mid-1990s.

7. The government has known about the risk of these cases following the related case of ICI v Colmar in 1999, and has failed in subject Treaty renegotiations and the EU Constitution to confirm that EU authority does not extend to direct tax laws of Member States. The government has sought to introduce measures to limit how far back legitimate claims can be made, some of which may also be illegal under EU law.

8. The government has been forced to change transfer pricing rules (Introduction of UK-UK transfer pricing in 2004) to fit with the ECJ’s decisions, causing a considerable administrative strain on business. Other member states have changed their transfer pricing rules so they do not apply to intra-EU transactions.

9. In PBR 2005 on 5 December 2005 confirmed that both the Film Tax Credit and Leasing corporate taxation rules will be changed. The government gave almost no attention to the fact that both these changes have come about in order to fit UK tax law within EU rules.

10. The European Commission has a Common Consolidated Corporate Tax Base Working Group, presently seeking to determine and implement a Common Consolidated Tax Base across the EU.

For further information contact:

Robert Oulds

Director

The Bruges Group

216 Linen Hall, 162-168 Regent Street, London W1B 5TB

UK

Tel: +44(0) 20 7287 4414

Fax: +44(0) 20 7287 5522

Mobile: 0774 002 9787

E-mail: info@brugesgroup.com>